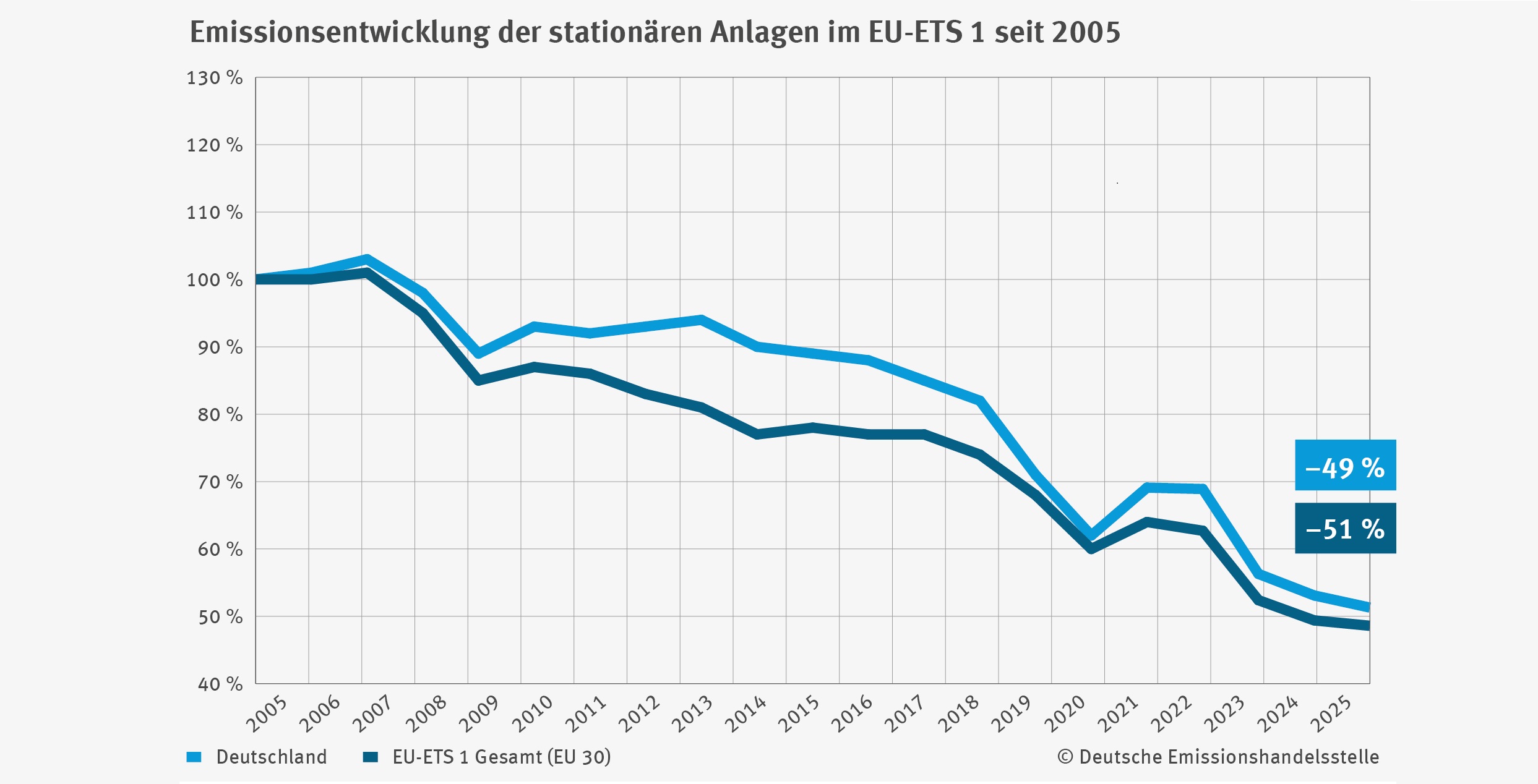

European Emissions Trading: German emissions to fall by around 3 percent in 2025

In 2025, Germany's 1,794 stationary industrial and energy installations emitted around 264 million tonnes of CO2 equivalents under the European Emissions Trading Scheme 1 (EU ETS 1). This is around 3.2 per cent less than in the previous year. In 2024, the decline in emissions from stationary installations was still 5.5 per cent. Emissions from aviation fell by 2.2 per cent in 2025 to around 8.8 million tonnes of CO2 equivalents (following a 16 per cent increase the previous year). This is reported by the German Emissions Trading Authority (DEHSt) at the Federal Environment Agency (UBA).

The EU ETS 1 covers stationary installations in the energy and industrial sectors, as well as intra-European air and sea transport. The emissions situation is largely determined by stationary installations. There are significant differences between the industrial and energy sectors. Emissions from the industrial installations covered by the scheme were 5.5 per cent below the previous year’s figure in 2025. This decline is largely attributable to the continued weak economic performance. By contrast, the fall in emissions from energy installations was only around two per cent, representing a significant slowdown (9.5 per cent in the previous year). A similar picture emerges at European level: According to the European Commission, emissions from stationary installations in the EU ETS 1 fell by around two per cent (6.5 per cent in the previous year). Emissions from aviation rose by around one per cent.

“Since its introduction in 2005, emissions trading has gradually developed into the key climate protection instrument in Germany and Europe," says UBA President Dirk Messner. "Reported emissions have roughly halved over the last 20 years. However, progress towards climate neutrality has slowed, as demonstrated by the more modest reductions in emissions in recent times. In particular, it is clear that the progress made in climate protection within industry in recent years is largely attributable to weak economic performance – not to a shift towards low-emission production. This must be taken into account in the reform of the emissions trading scheme, which is due to start this summer. As part of a robust mix of policy instruments, the emissions trading scheme can become the driving force behind a modernisation agenda for European and German industry.”

Christoph Kühleis, acting head of the ‘Climate Protection, Energy and German Emissions Trading Authority’ division at the UBA, adds: “The targeted use of auction proceeds from emissions trading is a key element on the path to climate neutrality. For the transformation of industry, the electrification of industrial processes, the use of green hydrogen and low-carbon production methods – such as direct reduction in the steel industry – are of particular importance. The roll-out of these technologies and the development of the associated infrastructure are not yet progressing quickly enough. Emissions trading can and should place greater emphasis on this in future.”

Emissions from energy supply

Emissions from energy supply fell by around two percent in the reporting year 2025 to approximately 167 million tonnes of CO2 equivalents. Although this marked the lowest level since the start of the EU ETS 1 in 2005, the year-on-year decline in emissions has slowed significantly. The main reasons for this trend over the past year are the noticeable increase in electricity generation from photovoltaic systems and the decline in electricity generation from lignite-fired power stations. At the same time, higher emissions from hard coal and natural gas power stations, a decline in hydropower and wind power generation, and a reduction in the negative electricity exchange balance (net imports have fallen) tempered this effect. The share of renewable energies in gross electricity consumption in Germany stood at around 55 percent in 2025, representing only a minimal increase compared with the previous year.

Industrial emissions

Emissions from energy-intensive industrial installations covered by the EU ETS 1 fell by around five percent to approximately 97 million tonnes of CO2 equivalents. The declines were particularly marked in the iron and steel industry, in industrial and construction lime, and in the paper and pulp industry. This trend is primarily driven by falls in production. Emissions from the 92 industrial installations that have been subject to emissions trading since 1 January 2024 following the amendment of the European Emissions Trading Directive (Directive 2003/87/EC) amounted to around 370,000 tonnes of CO2 equivalents and are included in the total emissions from stationary installations. However, as these are predominantly installations with no or only very low emissions, they have only a minor impact on the overall trend.

Emissions from aviation

Emissions from aircraft operators administered by Germany fell by around two percent in 2025 to around 8.8 million tonnes of CO2 equivalents. The upward trend that began in 2021 has thus come to an end for the time being, and emissions remain at the pre-pandemic level of 2019. Aviation has been integrated into the EU ETS 1 since 2012.

Emissions from maritime transport

Given that implementation in the maritime sector is still in its early stages – it has only been part of the EU ETS 1 since 2024 – the data available remains limited. Shipping companies often submit their emissions reports only shortly before the statutory reporting deadlines expire, which delays the analysis. Against this background, no reliable data is currently available for 2025 on the emissions from ships and shipping companies administered by Germany. In 2024, around 640 shipping companies administered by Germany reported approximately eleven million tonnes of CO2 equivalents under the EU ETS 1.

Emissions Trading and Total Emissions

Germany’s total emissions across all sectors for 2025 remained virtually unchanged compared with the previous year. According to provisional figures from the UBA, emissions amounted to 649 million tonnes of CO2 equivalents (-0.1 percent compared with 2024). The slight declines in emissions within the EU ETS 1 are offset by increases in emissions in the buildings and transport sectors.

The analysis of the emissions situation under the National Emissions Trading Scheme (nEHS) for 2024, which has now also been finalised, shows emissions levels to be virtually unchanged compared with the previous year. This means that the nEHS cap was significantly exceeded for the first time. The nEHS covers all fuels outside the EU-ETS 1, in particular the buildings and transport sectors. Together, the nEHS and EU-ETS 1 regulate over 85 percent of Germany’s greenhouse gas emissions.

Associated content

Links

- Reports on the emissions situation in the EU ETS 1 up to the reporting year 2025

- Reports on the emissions situation in the nEHS up to 2024

- Greenhouse gas data reveals the need for fresh momentum in climate action

- Further information on the auction under ETS 1

- How does ETS 1 work?

- The National Emissions Trading Scheme explained