Extreme weather events can damage a building’s envelope and the interior of a building. Typical storm damage to buildings includes torn-off roof tiles and ripped-off parts of cladding as well as broken glass panes in windows or doors. Indirectly, buildings can be affected by fallen or broken trees and masts or by damage to buildings in the neighbourhood. Depending on their size, hailstones can have enormous powers of impact capable of damaging roofs, photovoltaic units, window panes or facings. Especially if water penetrates to the interior of buildings – either due to floodwater or heavy rain – this can also cause considerable damage in interior rooms of buildings, in particular to household effects. As a result of such events, the highest single claims for damage to a one-family house, can be as high as 100.000 Euros; but in particularly extreme cases such as the flooding disaster in 2021, an individual damage to a one-family home can total ten times that amount.142

As far as the development of frequency and intensity of heavy rain events and storms is concerned, it has not been possible so far to identify a clear trend for Germany. Likewise – contrary to temperature predictions – pertinent projections for the future are still fraught with problems. As far as regional climate models are concerned which were examined by the network of experts linked to the BMDV, it is possible to discern a slight decrease in extreme wind speeds, especially in summer. However, these changes are negligible, whilst statements on wind speed should, on principle, be viewed with caution.143 Whether storms such as Hurricane Frederike experienced in the winter of 2017/2018 will occur more frequently or more intensely in future, is therefore currently impossible to predict with certainty for Germany. However, as far as heavy rain is concerned, climate researchers expect more frequent and more extreme cases of heavy precipitation in Germany in future (cf. Indicator BAU-I-4).

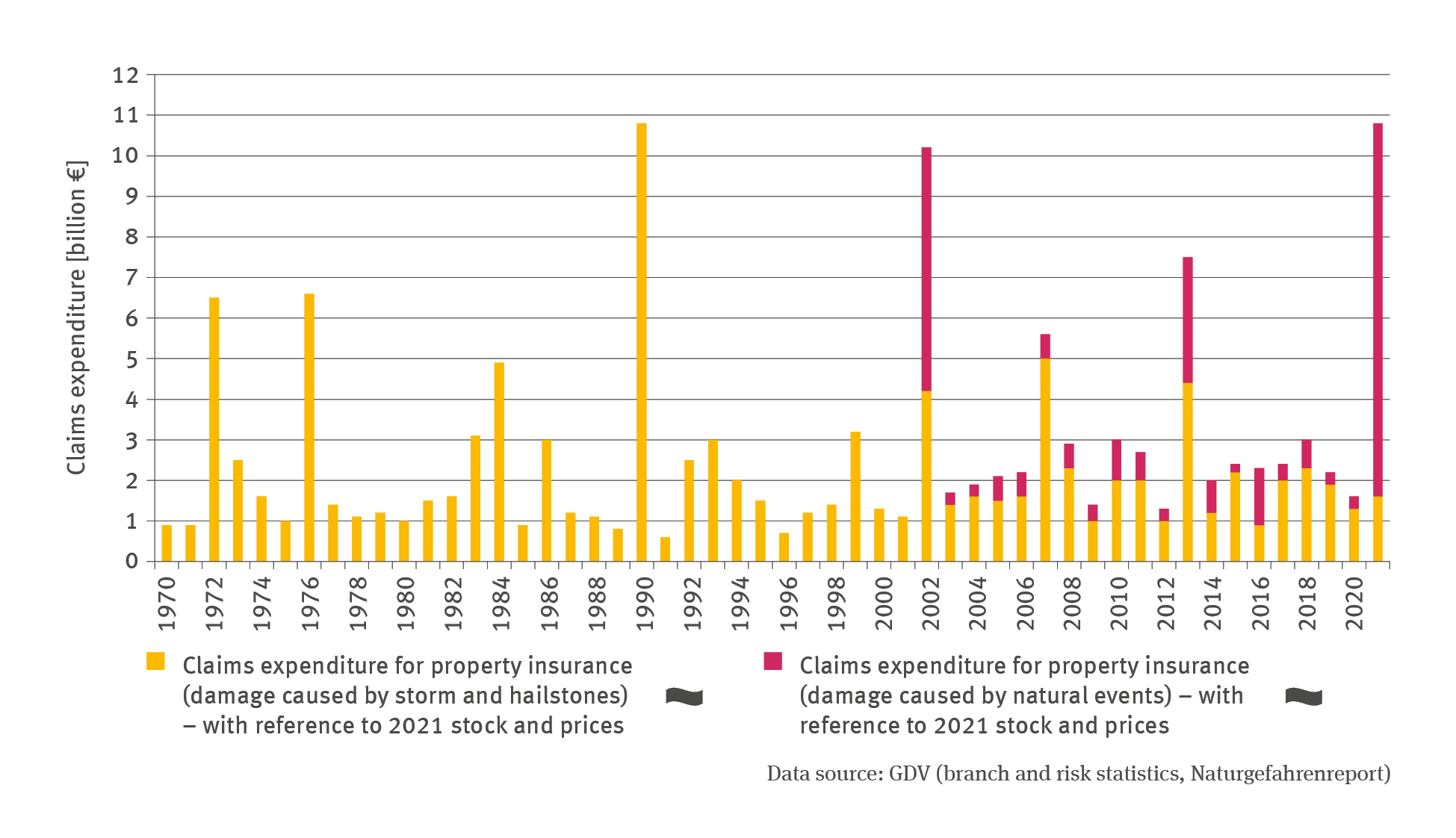

The extent of damage to buildings and their interiors caused by extreme events is reflected by the amounts of money involved in claims settled by the insurance industry. In particular with regard to high insurance densities as for instance in the insurance of private buildings against storm and hailstorm damage (in view of 95 % density, it would be correct to speak of near-saturation of the market), even regionally limited damage events are reflected well in statistics. Any change in reported claims and associated damage – settled by insurance companies with policyholders – can therefore be linked directly to changes in the frequency and intensity of damage events.

In respect of damage covered by customary property insurance, the amounts claimed due to fire, lightning strike, explosion and tap water have remained more or less consistent over the years. In cases of storm and hail damage and other natural hazards, caused by earthquakes, landslides, subsidence, snow pressure or avalanches as well as flooding due to a river breaking its banks or heavy rain, damage amounts fluctuate strongly from year to year. In some years damage events can be cumulative as a function of weather patterns, and some particularly violent events can cause major damage. By comparison, other years are relatively ‘quiet’.

Included in claims expenditure for property insurance – apart from private residential buildings and their household effects – are also commercial and industrial premises and associated contents as well as operational interruptions due to damage events. This expenditure covers payments and provisions for any damage caused in the relevant business year including any expenses for claim settlements. Regarding the time series, the stock and prices valid in 2021 were extrapolated in order to offset any inflationary effects or changes regarding the stock insured and to permit a comparison of the figures recorded for individual years.

The time series examined with regard to claims expenditure for property insurance has so far not shown any significant trend either for damage from storm, hailstones or other natural hazards. However, from time to time there are years when individual extreme events push up the claims expenditure. After the turn of the millennium this applies in particular to 2002 when the August floodwater as well as several hurricanes (especially Hurricane Jeanett) caused massive damage. In January 2007, the low-pressure system, known as Hurricane Cyril, affected public life in large parts of Europe claiming 47 lives in Europe as a whole. In 2013 there were as many as five major hailstorms which pushed up the total amount of claims: Manni and Norbert in June, Andreas and Bernd in July as well as Ernst in August. The flooding in June of that year – extrapolated to the stock and price information for 2021 – caused losses amounting to 2.38 billion Euros. In January 2018, the low-pressure system known as Hurricane Friederike caused damage in Germany totalling 900 million Euros.

The highest claims expenditure in terms of property insurance for damage from natural hazards in Germany so far, occurred in July 2021 as a result of the water masses deposited by the low-pressure system known as Bernd, in a two-day period, on the Rhineland-Palatinate and North Rhine-Westphalia. This caused insured material damage to residential property, household effects and business premises totalling 8.1 billion Euros.144

142 - GDV – Gesamtverband der Deutschen Versicherungswirtschaft e.V. (Hg.) 2022: Naturgefahrenreport 2022. Zahlen, Stimmen, Ereignisse. Berlin, 58 pp. https://www.gdv.de/resource/blob/105828/0e3428418c45df-91f7ee5f280a5a9bff/download-naturgefahrenreport-2022-data.pdf.

143 - Brienen S., Walter A., Brendel C., Haller M., Krähenmann S., Rauthe M., Razafimaharo C., Stanley K., Höpp S., Rybka H., Ganske A., Schade N., Möller J., Jensen C., Jochumsen K., Nilson E., Fleischer C., Helms M., Rudolph E. 2020: Klimawandelbedingte Änderungen in Atmosphäre und Hydrosphäre: Schlussbericht des Schwerpunktthemas Szenarienbildung (SP-101) im Themenfeld 1 des BMVI-Expertennetzwerks. 157 pp. doi: 10.5675/ExpNBS2020.2020.02.

142 - GDV 2022, cf. endnote no. 142.