By now, taking out homeowners insurance for storm and hailstone damage is almost a matter of course among homeowners. By contrast, the necessity to conclude insurance contracts for other extreme natural hazards such as heavy rain and floodwater has not yet met with broad acceptance even though precisely in respect of these hazards it is feared that there will be an increase owing to climate change, and that heavy rainfall events are bound to occur regardless of location. Such events can therefore happen anywhere causing damage to a homeowner’s building and household effects.

In past cases of damage both private individuals and traders who incurred the damage, used to receive government and non-governmental aid. This happened for instance after the extreme floodwater event in August 2002 which caused damage totalling more than 11 billion Euros. Only some of these premises were insured. A trust was set up entitled ‘Reconstruction Aid’ (Aufbauhilfe) for reconstruction and damages. The Trust was financed with 3.5 billion Euros from federal funds and from 3.6 billion Euros from Länder funds. From these amounts, 923 million Euros alone were awarded to the refurbishment of damaged residential buildings and for the replacement of damaged or destroyed components of buildings. The damage caused by floodwater in June 2013 in which the Länder of Saxony-Anhalt, Saxony, Bavaria and Thuringia were most affected, amounted to approximately 8 billion Euros. In this case the Federal Government and the Länder awarded floodwater aid amounting to 3.7 billion Euros for the Länder in the central part of Germany.

In view of the considerable sums spent on floodwater aid and because government aid cannot cover all privately incurred damage, the Federal Government is appealing to homeowners and tenants to make largely their own provisions thus reducing both the damage incurred and the demands made on government aid. Any person who might at some stage become affected by floodwater is legally obliged to take the necessary precautionary measures. In addition to structural measures, it is part of this personal provision to make sure, above all, that adequate insurance cover is in place. In 2017 the Minister-Presidents of the Länder agreed that in future only those homeowners can expect to receive aid beyond emergency relief, who had been unsuccessful in securing an insurance deal or if they had been offered a policy at economically unreasonable terms and conditions.

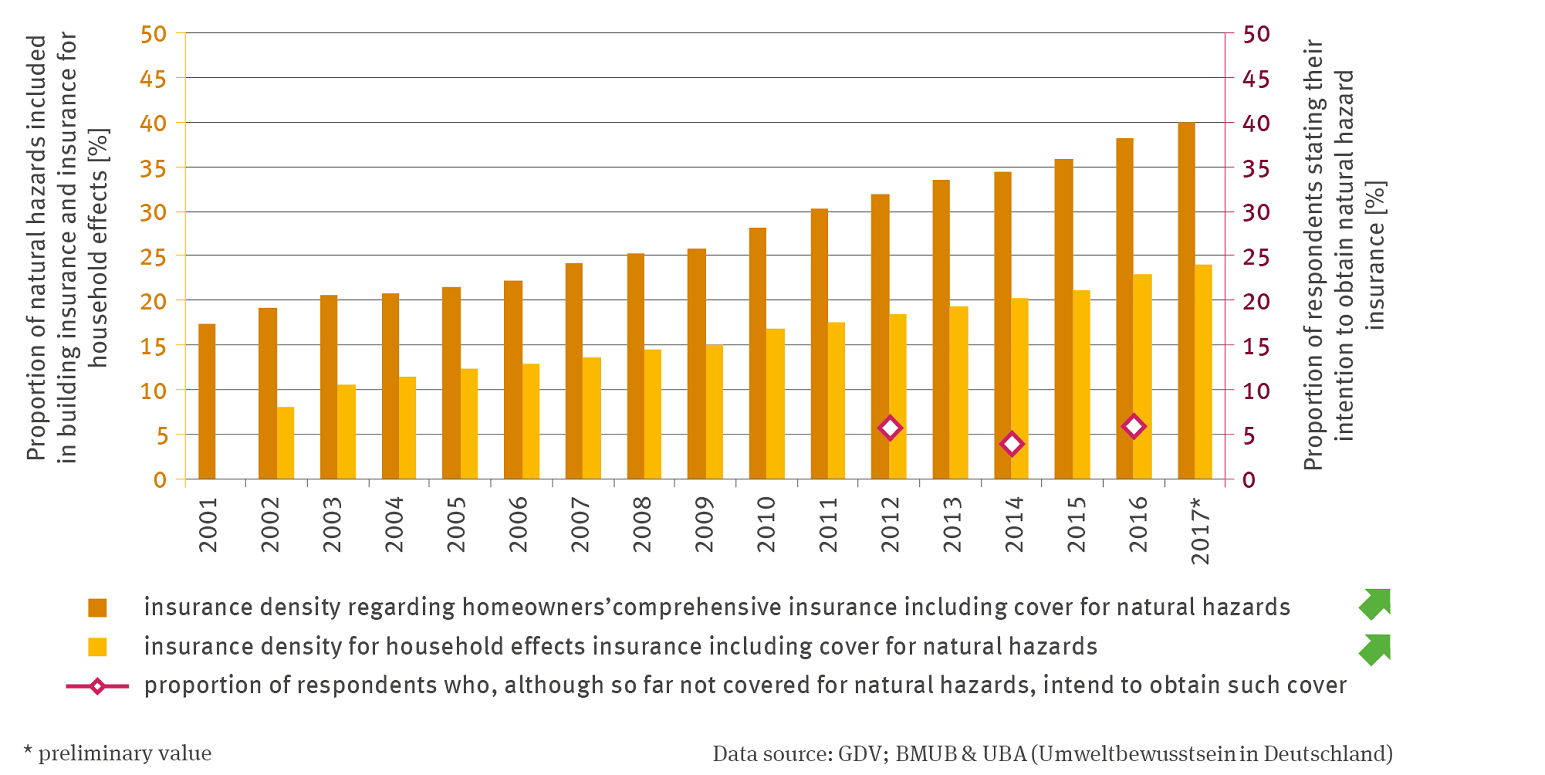

Extended insurance against natural hazards (eEV) – which covers so-called damage from natural hazards – is now acknowledged as a well-established product in the insurance market. However, by late 2018 only 43 % of residential buildings were covered by eEV. As far as tenants are concerned, it is relevant to conclude insurance policies covering household effects for damage caused by natural hazards, because damage to buildings – caused by natural hazards, especially if this damage occurs in rooms at ground level or in cellar rooms – can also be caused to a tenant’s household effects. By 2017, however, a meagre 24 % of all policies for household effects incorporated insurance cover for natural hazards.

Even if the number of policies concluded were to rise continuously, the awareness of the necessity to have eEV insurance has still not penetrated the consciousness of sufficiently large parts of the population. The hazards are underestimated by the public, and their knowledge regarding which kind of damage is actually covered by an insurance policy they may have concluded is woefully inadequate. In the past, extreme events used to produce a temporary surge in the public’s willingness to take out insurance cover. The outcomes of a representative public survey carried out every two years on behalf of the UBA, entitled Environmental Awareness in Germany (Umweltbewusstsein in Deutschland)I indicate that even for the next few years it is futile to expect any sharp rise in the density of insurance cover. In 2012 just under 6 % of respondents stated that although they had not yet concluded an eEV policy, they would like to conclude such an insurance policy in future. Two years later this percentage had declined to just 4 %. A recent survey carried out in 2016 resulted in an outcome of 6 %. It is therefore obvious that so far there is no distinct trend discernible.

In an effort to appeal to the public’s sense of responsibility and to promote an increase in personal provision, politicians, the insurance industry and consumer protection organisations in several federal states are all acting in concert. By late 2018, already ten Länder had implemented or started campaigns to inform the public and to inspire people to conclude appropriate insurance deals.

The underwriters are in a position to insure almost all buildings and homes in Germany and, most of them would also be able to offer cover for natural hazards at affordable prices. Exceptions are only made in respect of a few areas where the hazards are particularly great. But even in those cases individual insurance solutions can be found, i.e. by incorporating high elements of ‘excess’ (a pre-determined amount deducted from the total settlement received by the claimant) and higher, risk-congruent insurance premiums.

However, in addition to taking out insurance policies, every citizen ought to take the necessary precautions to protect themselves from potential damage. This includes taking measures with regard to construction and systems technology appropriate for the protection of homes (houses/ flats) both before, during and after an extreme event.

I - The representative population survey (of German-speaking residents aged 14 or more years) entitled Environmental Awareness and Behaviour in Germany (Umweltbewusstsein und -verhalten in Deutschland) (has been carried out every two years since 2000on behalf of the BMU and the UBA. Since 2012, questions were incorporated in the survey intended to supply data for the DAS monitoring indicators; from 2016 onwards, these questions were asked every four years in the environmental awareness surveys.