As a result of weather extremes, Germany’s plant production has repeatedly suffered some considerable yield losses in the course of recent years. A study carried out by the German Insurance Association (GDV) regarding insurance for agricultural multirisks (Landwirtschaftliche Mehrgefahrenversicherung) for Germany, estimated that annual harvest losses caused by weather-related risks in Germany between 1990 and 2013 amounted to roughly 510 million Euros per annum. 54 % of harvest losses in this period – that is to say, prior to the drought years of 2018 to 2020 – can be attributed to drought, 26 % of damage to hail storms and just 20 % to tempests, heavy rain, flooding or outwintering and frosts.108 If extreme events increase as a result of climate change, agriculture is liable to have its fair share of harvest damage or harvest losses. The drought summer of 2018 has demonstrated that the average yield losses mentioned above can sometimes be much more severe. Many agricultural businesses struggled to survive. The businesses affected obtained financial support totalling 340 million Euros from Federal and Länder sources109.

Typically any statements regarding weather-related harvest losses are made in terms of approximated values. Basically, the most reliable data on insured damage might be disclosed by insurance companies themselves, as funding disbursed from aid programmes on a case-by-case basis covers only part of the damage incurred. So far, however, only few agricultural businesses have comprehensive insurance protection from harvest losses which result from extreme weather events such as drought. According to a recent BMEL survey among German insurance companies in the years of 2020 to 2022, roughly just 1 % of arable ground in Germany was insured for drought. One reason for the hitherto low insurance density is the fact that insurance premiums continue to be very expensive. In particular drought, but frost too, are among the so-called accumulation risks, which means that several regions can be affected at the same time. The high amount of damage associated with such situations thus increases the premiums charged. In fact, in several EU member states, there has been government part-funding available for many years for multi-risk insurance policies, in order to make insurance premiums more affordable. Since multi-risk insurance for orchards and vineyards in Baden-Württemberg was first subsidised by state funding in Germany in 2020, the Länder of Baden-Württemberg, Bavaria, Thuringia and North Rhine-Westphalia currently provide subsidies including state and / or EU funding for multi-risk insurance policies in respect of specific crops and risks, covering up to 50 % of the insurance premium. For the first time in Germany, Bavaria in 2023 also subsidised multi-risk insurance for arable and grassland areas including the risk of drought. Lower Saxony, along with Bremen and Hamburg are planning to introduce funding for multi-risk insurance as of 2024.

Compared to multi-risk insurance, insurance for hailstone damage is already in wide-spread use in agriculture. More than two thirds of all farmland is insured for hailstone damage110. Regarding reports from hailstorm insurance companies in respect of expenditure insurance claims, it is therefore possible to make statements on at least part of the losses.

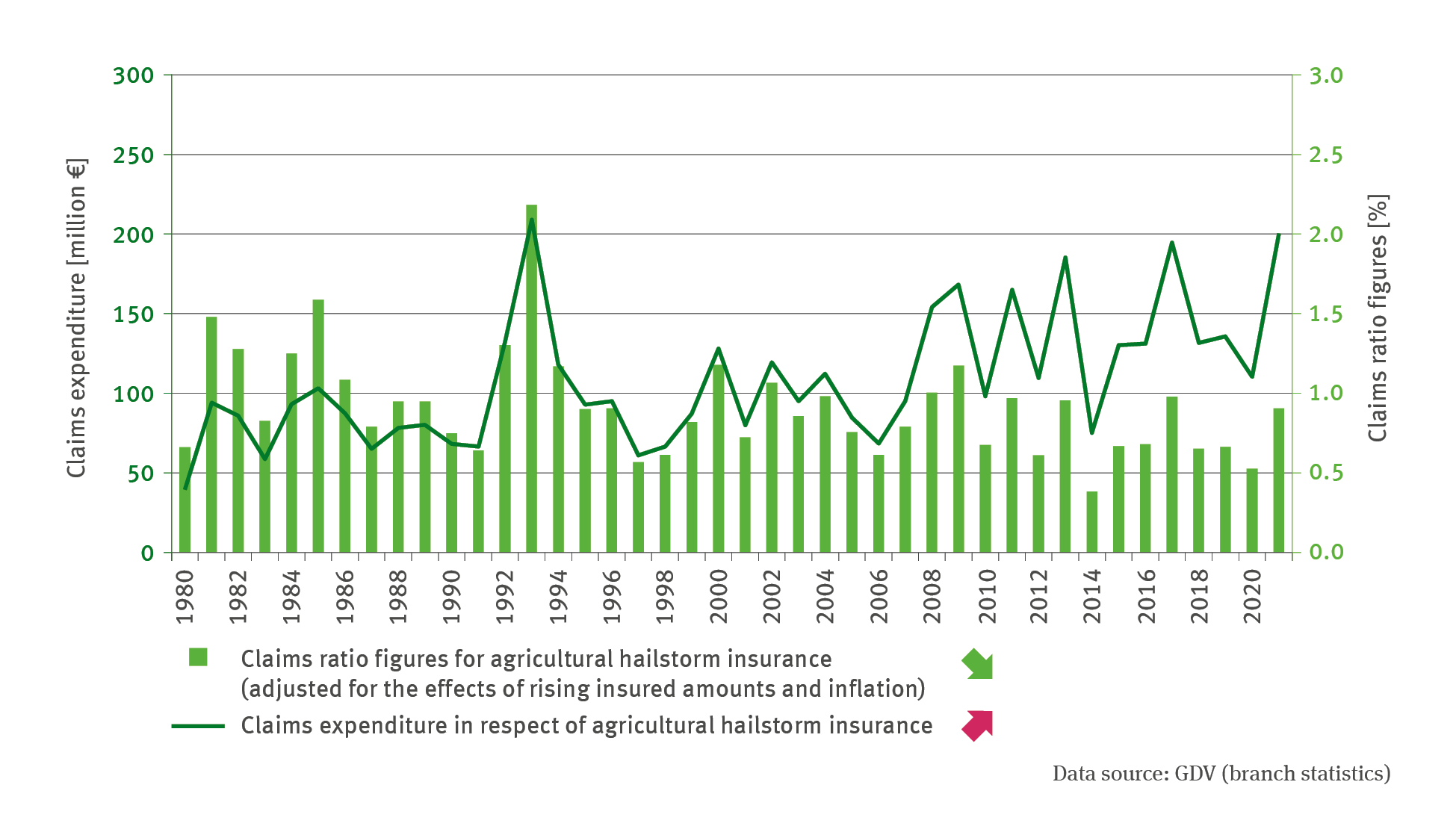

The claims expenditure, that is to say, the gross expenditure arising from insurance claims for hailstone damage, has increased significantly between 1980 and 2021. However, this is not exclusively due to increased incidents entailing claims. In fact, it is also a result of increases in insured amounts. In Germany, the market for agricultural hailstorm insurance is not considered saturated and the values insured are on the increase.

Contrary to claims expenditure, claims ratio figures for agricultural hailstorm insurance are adjusted for the effects of rising insured amounts and inflation. In order to infer some more direct conclusions, it is therefore possible to use the claims ratio figures to identify the driving force underlying the claim – in this case hailstorm events. The trend indicated for the claims ratio is falling. So far, 1993 was the year with the greatest incidence of damage during the period examined. In 2002 major hailstorms, especially in south-west and eastern Germany, caused total losses in many locations, while in 2009 the north and south were affected most severely between late April and mid-August by a sequence of thunderstorms of extraordinary violence. In 2017 there was substantial damage caused by changeable weather patterns with regional hailstorm events.

Despite some regionally substantial damage, 2018 was overall a year with comparatively moderate damage, although between the end of April and mid-June, not a day went by without damage being reported to hailstorm insurers. In the south and south-west of Germany, August hailstorms damaged maize crops just before harvest – a crop which, in that drought year, had still promised to deliver good yields. Likewise, in 2019 the great heat was accompanied by heavy thunderstorms. The month most affected by hailstone damage was June. Thunderstorm ‘Jörn’ which afflicted the south and south-east of Germany, brought some of the ten most severe hailstorms known to property insurers since 1997. Other hailstorm events in June in Lower Saxony and in July in Hesse, northern Bavaria, Thuringia, Mecklenburg-Western Pomerania, among others, struck many rapeseed, peas and cereal crops that were ready to be harvested at that time.

There were no major hailstorm events in 2020. In June 2021, however, thunderstorm supercells – these are rotating and very long-lasting thunderstorm clouds – emitted huge hailstones thus causing enormous damage, especially in agricultural areas of Baden-Württemberg and Bavaria. It is true that in 2021 the claims ratio in Germany nationwide was higher than in the three preceding years and also higher than the mean of the past 30 years. However, it was not as high as the peak values recorded for the 1980s and 1990s.

Although hailstorm insurance compensates agricultural businesses for tangible harvest losses, it does not cover any associated consequential losses incurred by an agricultural business as a whole. The insurance does not cover any losses in terms of market presence in a hailstorm year, or underused capacity of operational infrastructure or even increased expenditure arising from product harvesting and sorting efforts. This is another reason why many companies do not regard concluding a hailstorm insurance as their only option. Especially in orcharding, farmers increasingly use safety nets for product protection from hailstones.

109 - BMEL – Bundesministerium für Ernährung und Landwirtschaft 2018: Gemeinsame Dürrehilfe durch landwirtschaftliche Betriebe stark gefragt. Pressemitteilung Nr. 207/2018. https://www.bmleh.de/SharedDocs/Archiv/Pressemitteilungen/2018/207-duerrehilfe.html

110 - BMEL (Hg.) 2017: Extremwetterlagen in der Land- und Forstwirtschaft – Maßnahmen zur Prävention und Schadensregulierung. Berlin, 26 pp.